Updated March 20, 2025, at 2:13 PM

From the numbers above the gas pump to the price tag on eggs, evidence of inflation has long been visible in our daily lives, and the insurance industry is certainly no exception.

With auto insurance premiums increasing 6% in 2024 and rate hikes for home insurance predicted to reach anywhere between 6-23% in some states, inflation’s impact is top of mind for many clients.

Still, another area of insurance that clients may have never considered being impacted by inflation is their life insurance.

Life Insurance Awareness Month every September brings an opportunity to initiate conversations with clients and prospects about inflation—a topic that already has their attention—while revealing potential opportunities for improvement they didn’t know existed.

First, let’s examine how inflation is affecting retirement portfolios in general.

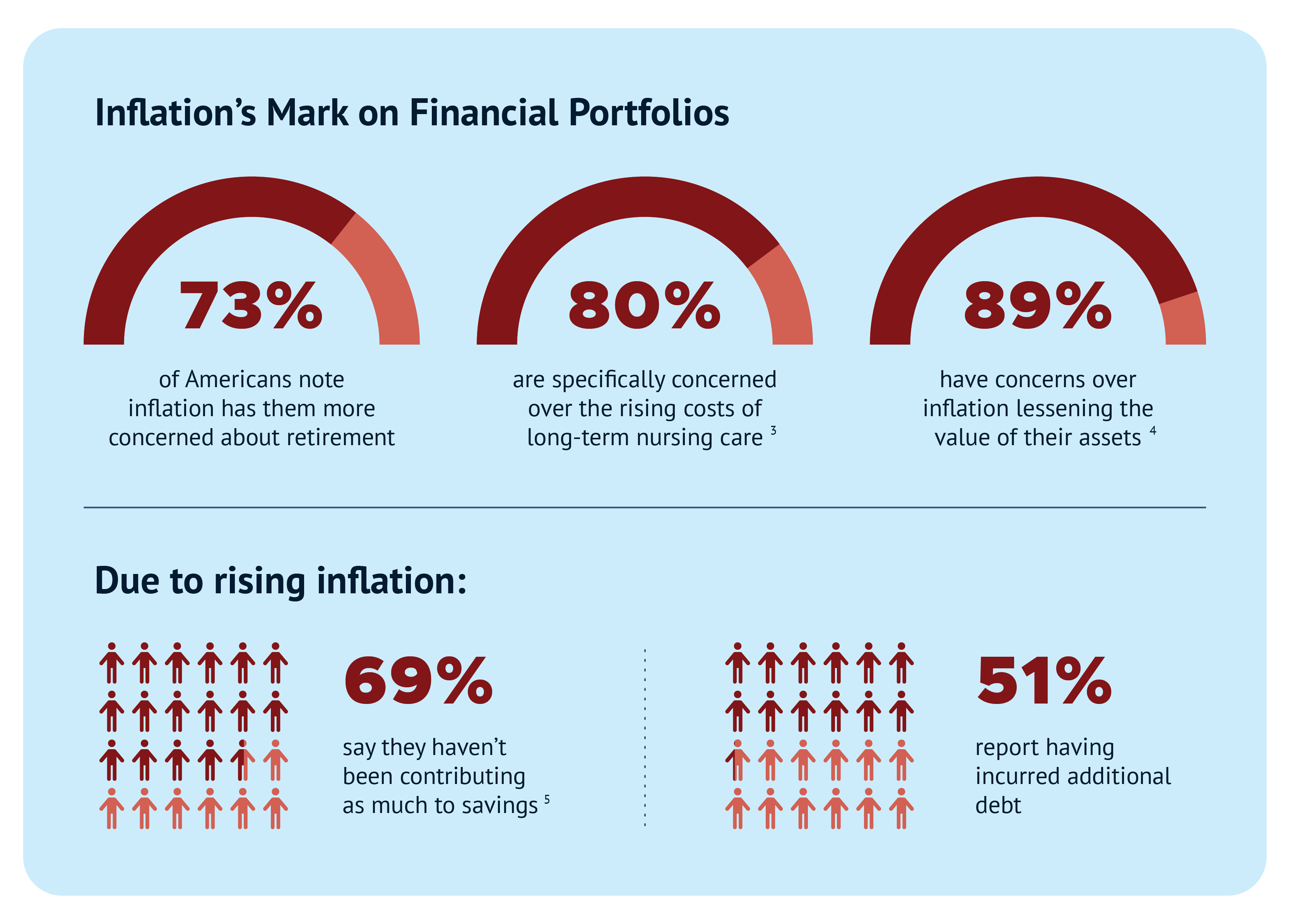

The Data Around “Inflated” Retirement Concerns

Looking closely at the statistics, it can be observed that as inflation raises prices, there’s a shift in the behavior of retirement savers.

There’s much to be said about inflation’s impact on a retirement portfolio, and while topics like estate planning and care planning are high on the client’s list of concerns, another important asset to highlight in conversations—which is also heavily intertwined with estate planning—is life insurance.

Related: Turn Stagnant Assets into Tax-Advantaged Care Planning Solutions

Inflation’s Hidden Mark on Life Insurance

When we talk about inflation’s impact on life insurance, what we’re addressing is the decrease in the purchasing power of the death benefit. To put it into perspective, a $1M face amount ten years ago is worth $825K in today’s dollars.

If you factor in a client’s potential income growth alongside the diminished purchasing power of the death benefit, you get a coverage shortfall that could significantly affect the beneficiaries.

Considering life insurance is likely one of the most significant assets in a client’s estate, financial professionals must ensure that it meets their needs throughout economic and life changes.

How Financial Professionals Can “Deflate” Concerns

Whether it’s divorce, the birth of a child, a career shift, or a significant health change, there are many reasons why it’s a good idea to regularly review in-force life insurance policies to ensure they still meet a client’s goals.

However, even if someone hasn’t undergone any life changes in the previous year, inflation is reason enough to analyze their current life insurance policy for coverage gaps. By evaluating the face amount relative to current inflation rates, you can offer guidance for adjusting coverage as necessary or explore policy options designed to hedge against inflation, such as indexed universal life insurance or other solutions.

It’s true: Individual policy reviews can be time-consuming. The good news is that two tools can dramatically streamline the process for financial professionals.

Introducing the Life Insurance Inflation Calculator

The new Life Insurance Inflation Calculator may be considered a financial professional’s secret weapon in revealing the impact of inflation on a client’s in-force policy. This quick, easy-to-use tool evaluates existing coverage and current income to identify protection gaps. After inputting a few details about a policy, you receive a straightforward output that can be presented to clients.

Utilizing the Life Insurance Inflation Calculator in your policy reviews can strengthen relationships with current clients and open doors for referrals. For example, after seeing the results from the calculator tool, clients may very well bring the experience up in conversation with family and friends when the topic of inflation arises, prompting new prospects to seek your guidance.

Leveraging the Comprehensive Analysis and Review Program

After revealing a potential coverage gap using the Life Insurance Inflation Calculator, the Comprehensive Analysis and Review (CAR) program is a practical next step to implement.

The program allows financial professionals to lean on a team of experts to handle all the heavy lifting associated with a life insurance policy review. The team can gather in-force illustrations with signed authorization and analyze its current performance against today’s marketplace. Then, a snapshot presentation with suggestions for suitable alternatives (if applicable) is provided for an easy conversation with clients.

Related: Life Insurance Policy Reviews for Clients [CAR Overview]

Jumping at Life Insurance Awareness Month Opportunities

September offers financial professionals a unique opportunity to educate clients and prospects about the necessity of reviewing their coverage. Efforts can be as large as hosting a webinar or information luncheon about inflation or as simple as sending a personalized email to clients offering to conduct a free policy evaluation.

If you’d like to arm yourself with the Life Insurance Inflation Calculator, Comprehensive Analysis and Review program, or other tools to aid in these powerful conversations, contact our team today!

Sources From Graphic:

3. https://www.forbes.com/sites/dandoonan/2024/04/11/americans-are-worried-about-retirement-savings-and-they-should-be/

4. https://www.schroders.com/en-us/us/institutional/media-center/schroders-retirement-study-finds-inflation-taking-toll-on-retirees/

5. https://www.allianzlife.com/about/newsroom/2024-Press-Releases/Americans-Reducing-Retirement-Savings-and-Taking-on-Debt-Due-to-Inflation